Swiss private account study 2026

If you would like to receive a detailed overview of the Swiss private account study 2026, simply enter your email address in this field and click on “Request free PDF”.

The Swiss private account study from online comparison service moneyland.ch reveals huge differences between banks. While the services provided are similar across all Swiss banks, the costs differ enormously. While “free accounts” are offered by some banks, the total annual costs at other banks can be as high as 240 francs.

A private account is part of everyday life. Most people receive their salaries and pensions through their private account. You can also use a private account to pay bills, and use a linked debit card to pay for purchases and to withdraw money at ATMs.

Because private accounts are such a major part of everyday banking, moneyland.ch carried out a study of Swiss private accounts, accounting for bank transfers and debit cards. A total of 34 different Swiss banks were included in the analysis, with neobanks and some regional banks represented in addition to major banks with a countrywide presence. The study shows the differences between private accounts, and the costs that apply.

Are there differences between private accounts from different banks?

The palette of services included is largely identical, with very differences between Swiss banks.

Incoming and outgoing bank transfers, as well as payments and cash withdrawals with a debit card, are standard services included in all Swiss private accounts. All but a handful of private account offers include eBill payment solutions and a custom Twint app.

Depending on your personal banking needs, there are other factors that may also be relevant. For example, there are differences between the online and mobile banking solutions from various banks. Your expectations with regards to customer service and the locations of your bank’s branch offices and ATMs also play a role. The moneyland.ch study does not account for these personal considerations.

Instant payments are still only offered by a few Swiss banks

One point on which Swiss private accounts do vary is instant payments. Around two thirds of the banks included in the analysis do not provide this service. Only 11 of the 34 service providers give you the option of making instant transfers to other Swiss bank accounts. On the other hand, receiving instant transfers is possible, as most Swiss banks are required to immediately credit instant payments to your account.

The neobanks Alpian, Neon, and Zak provide fast transfers, but only between their own accounts.

How much do Swiss private accounts cost?

Die Kosten eines Privatkontos hängen auch von der Nutzung ab. Für die Studie hat moneyland.ch zwei Profile erstellt:

The total cost of a private account varies depending on your banking needs. For its study, moneyland.ch calculated the costs for two different user profiles:

For both profiles, calculations are based on these joint assumptions: The customer pays their bills using online banking (10 outgoing bank transfers per month), uses digital bank statements only, and holds an average of 8000 francs in balances at the bank that hosts their private account.

For each user profile, moneyland.ch made two separate cost analyses: The costs of using the account for local transactions in Switzerland only, and the costs of using the account for a mix of local and international transactions.

You can find the results of the study, with detailed comparisons, in the PDF.

If you would like to receive a detailed overview of the Swiss private account study 2026, simply enter your email address in this field and click on “Request free PDF”.

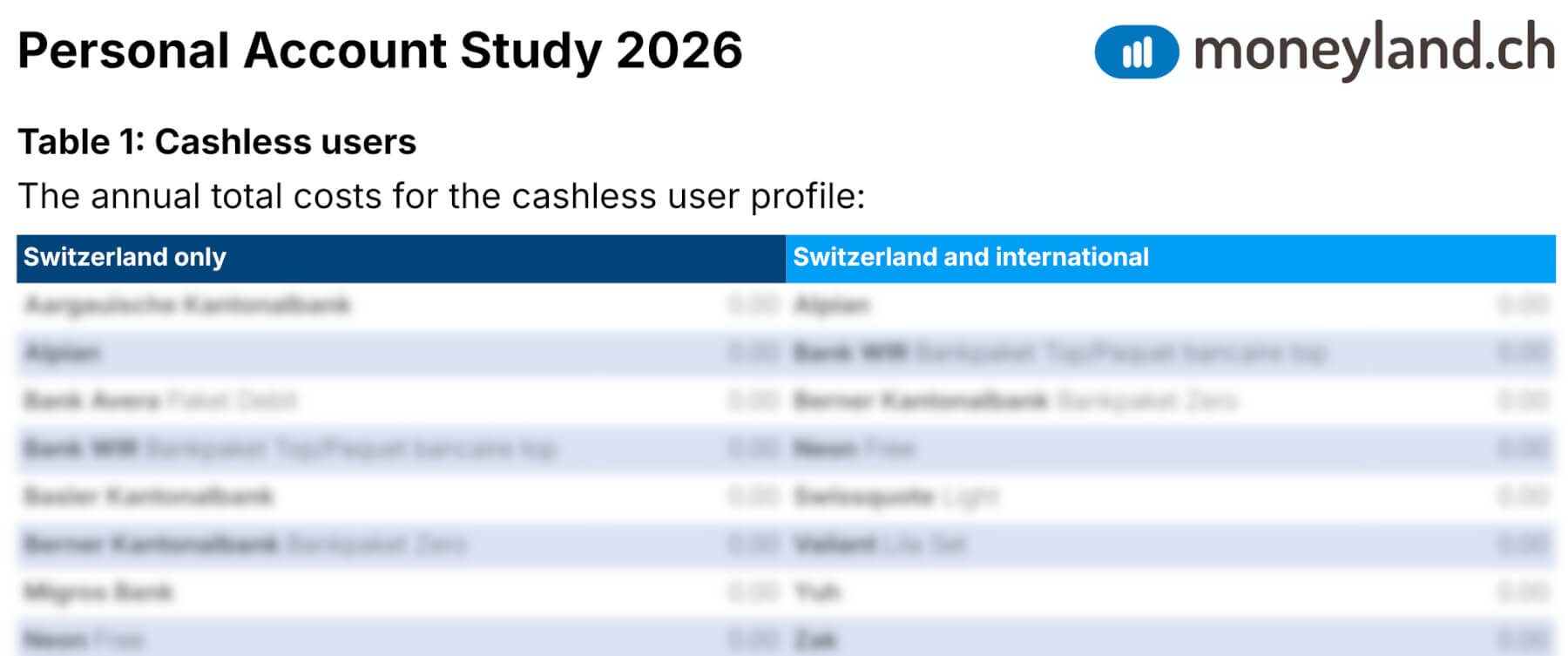

The total costs for Switzerland-only cashless users

There are 14 banks for which the total costs come to zero francs per year for this profile: Aargauische Kantonalbank, Bank Avera, Basler Kantonalbank, Bank WIR, Berner Kantonalbank, Migros Bank, Swissquote, UBS Key 4, and Valiant, as well as the neobanks Alpian, Neon, Yuh, and Zak.

The reason for the low costs is that some banks now offer private accounts with no basic, ongoing fees. Some of these also do not charge a basic fee for the debit card. “Until recently, only a handful of service providers offered private accounts without basic account fees. But that has changed since the Zürcher Kantonalbank moved to the no-basic-fee pricing model, with other banks like UBS Key 4 and Valiant following suit,” says Ralf Beyeler from moneyland.ch. “The competition from Revolut and other neobanks is likely part of the reason for this change,” adds Beyeler.

But most Swiss banks still charge basic account fees. The total yearly costs for bank customers who match the Switzerland-only cashless user profile are 48 francs at Raiffeisen and 60 francs at Postfinance. Standard private accounts from UBS take the last place with total costs of 144 francs per year.

The total costs for Switzerland and international cashless users

After accounting for foreign transaction fees, there are eight banks with total costs of zero francs per year: Bank WIR, Berner Kantonalbank, Swissquote, Valiant, and the neobanks Alpian, Neon, Yuh, and Zak. The total costs are higher at other banks. The total yearly costs for customers matching this user profile are 37.50 francs at the Zürcher Kantonalbank and 52.50 francs at Migros Bank. Raifffeisen and Postfinance both have total costs exceeding 100 francs per year.

Only 12 banks do not charge any foreign transaction fees for debit card payments in other countries. All of the other banks included in the study charge foreign transaction fees. Many banks charge a fee of 1.50 francs per payment. Percentage-based fees equal to 1 or 2 percent of the transacted amount are also common.

“When making payments outside of Switzerland, make sure to use a card that does not have foreign transaction fees. The card should also have favorable currency exchange rates,” recommends Beyeler. It is important to note that due to a lack of available information moneyland.ch was not able to account for currency exchange rates in the private account study. A recent analysis shows that markups on currency exchange rates can easily add a cost of two percent or more.

The total costs for Switzerland-only cash users

Bank Avera is the only analyzed bank where the total annual cost for the cash user profile is zero francs. The neobank Yuh takes second place, with total costs of 15.20 francs per year. Third place is shared by Caisse d'Epargne d'Aubonne and Sparkasse Schwyz, with total costs of 30 francs each.

“It is interesting to see that nearly all of the regional banks included in the study are in the top half of the list,” says Ralf Beyeler. One of the reasons is that although most regional banks charge a basic annual fee for their debit cards, they do not charge additional fees for each cash withdrawal.

The big banks are generally expensive for this profile. The total annual costs come to 36 francs at UBS Key 4, 48 francs at Valiant, 84 francs at Raiffeisen, and 120 francs at Postfinance. Standard private accounts from UBS take the last place, with total costs of 180 francs per year.

The calculations are based on a total of 60 cash withdrawals per year. For banks with their own ATMs, the calculations assume that half of the cash withdrawals are made at the bank’s own ATMs.

The total costs for Switzerland and international cash users

For a cash user who also makes 12 cash withdrawals at foreign ATMs, the cheapest bank is Valiant, with total costs of 48 francs per year. Next in line are Bank Avera with total costs of 60 francs, and Yuh with total costs of 74 francs. UBS Key 4 has total costs of 96 francs for this profile. Migros Bank, Postfinance, and the Zürcher Kantonalbank all have total costs of 120 francs per year. UBS takes the last place with total costs of 240 francs.

Which cantonal banks have the lowest total costs?

24 of Switzerland’s 26 cantons have their own cantonal banks. The analysis reveals huge differences between cantons. The cantonal banks of Basel-Stadt, Zurich, Aargau, and Bern have the cheapest private accounts. Those of Basel-Landschaft and Geneva are the most expensive cantonal banks for all four profiles. The differences between the cheapest and the most expensive cantonal bank fall between 100 and 135.50 francs, depending on the profile.

You can find the detailed results of the 2026 Swiss private account study in the PDF.

If you would like to receive a detailed overview of the Swiss private account study 2026, simply enter your email address in this field and click on “Request free PDF”.

Methodology

For the study, online comparison service moneyland.ch only included private accounts from Swiss banks, and accounted for financial transactions and debit cards. Other banking products like savings accounts, retirement saving accounts, and credit cards were not accounted for.

The following costs were accounted for:

For both the cashless and cash user profiles, the calculations are based on these assumptions.

These 34 Swiss service providers are included in the study: