Swiss Credit Card Study 2026

Get a detailed overview of the Swiss Credit Card Study 2026.

The differences between Swiss credit card offers in terms of the total cost are very large. Which credit card is cheapest largely depends on how you use credit cards. That is especially true for purchases from foreign merchants. For the Swiss Credit Card Study 2026, moneyland.ch analyzed numerous Swiss credit cards. The evaluation accounted for basic annual fees, reward programs, foreign transaction fees, and markups on currency exchange rates.

Credit cards are very popular in Switzerland, with a total of 8.4 million Swiss credit cards in circulation. Every year, Swiss credit cards are used to pay for nearly 59 billion francs of purchases, of which around 25 billion are purchases from foreign merchants.

Although credit cards are a product that most people use every day, many Swiss consumers hardly pay attention to the costs. The moneyland.ch Swiss Credit Card Study 2026 analyses the costs to find out which credit cards are the cheapest to use. The study determines the total annual costs, accounting for rewards, based on two different user profiles. Markups on currency exchange rates are also accounted for in calculations. The analysis does not include special promotional offers.

Credit cards with and without annual fees

Many Swiss consumers only use credit cards as a payment service for settling purchases of goods and services. But many credit cards include other services as well. The selection of credit card offers from Swiss issuers is broad and varied, with many credit cards also coming with insurance, airport lounge access, and other services in addition to payments. For that reason, consumers should consider if they only need payment services, or if they could also benefit from other services.

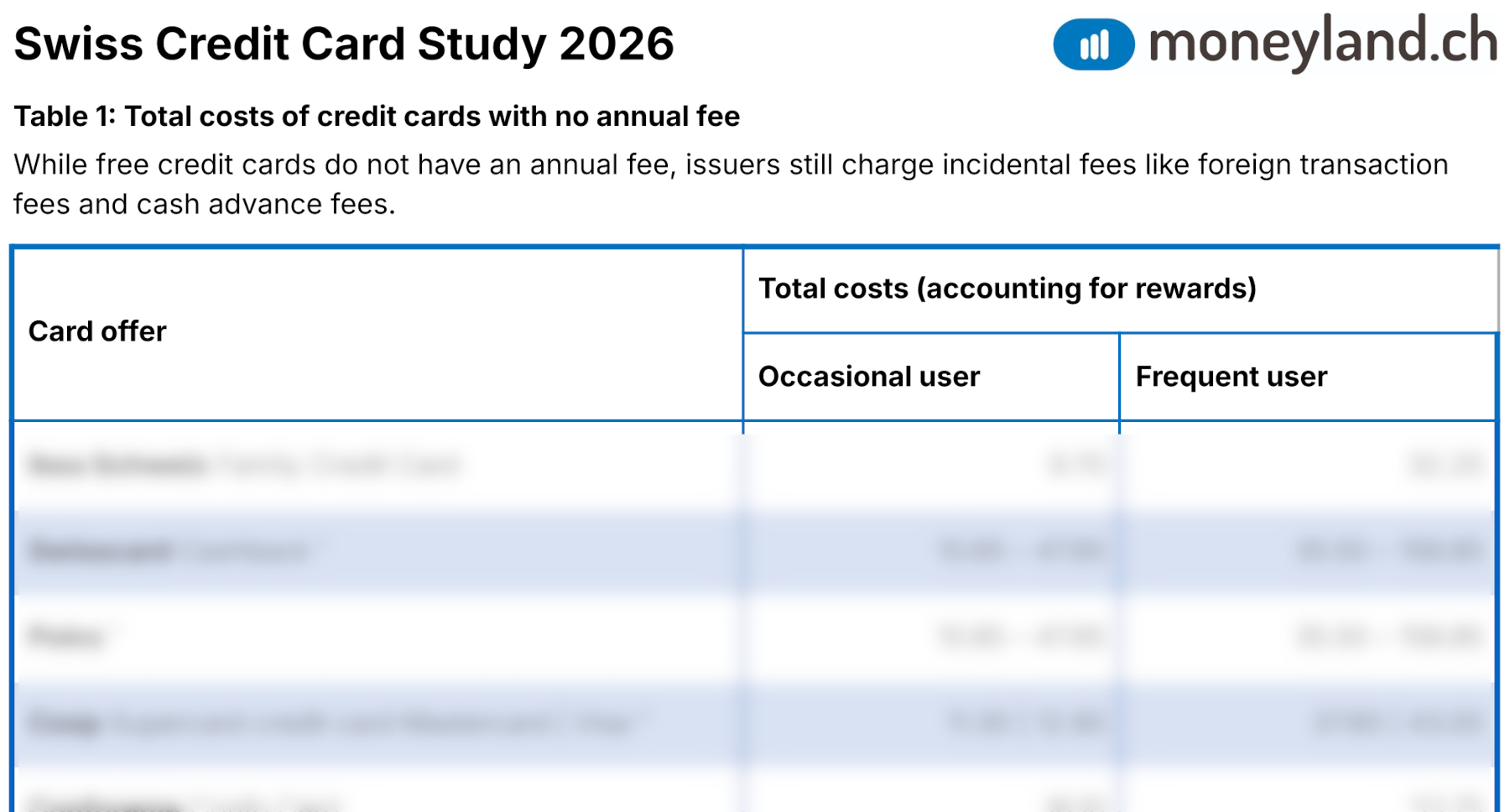

Credit cards with no annual fee

Credit cards with no annual fee are a good fit for consumers who only use credit cards for payments. Among others, no-annual fee credit cards are offered by popular retailers like Coop, Ikea Switzerland, Manor, and Migros. Most no-annual-fee credit cards come with reward programs that let you earn points or cash back for purchases.

“The term free credit cards is often used, but it is not an accurate description because you still pay incidental fees for foreign transactions and cash withdrawals at ATMs,” clarifies moneyland.ch personal finance expert Ralf Beyeler. The only difference to other credit cards is that you do not pay a basic monthly or annual fee for the credit card account.

For consumers matching the occasional user profile, the Ikea Family credit card is the cheapest, with costs totaling 9.70 francs per year. The foreign transactions included in the profile generate costs of 59.20 francs, of which 38.05 francs are made up of currency exchange rate markups. But the user would earn 49.50 francs worth of Ikea vouchers as rewards for their spending, which offsets the costs.

For consumers matching the frequent user profile, the total cost of using the Ikea credit card is 32.25 francs.

The detailed results are shown in table 1 of the PDF overview.

Get a detailed overview of the Swiss Credit Card Study 2026.Swiss Credit Card Study 2026

Right behind the Ikea card are the Cashback and Poinz bundles from Swisscard. However, only the American Express cards in these bundles qualify for second place. The accompanying Mastercard and Visa cards have much lower rewards to offset the costs, so the total costs are higher. The higher costs of these accompanying cards are also shown in the table.

Credit cards with annual fees

If insurance cover and other services are important to you, then cards with annual fees are worth looking at. Swiss issuers typically divide these paid cards into standard and gold offers, with some using a platinum category as well.

It is important to note that there are no fixed definitions of what constitutes a standard, gold, or platinum credit card. Each issuer decides on the services and benefits themselves. For example, Some issuers include comprehensive travel insurance in their standard credit cards, while others reserve this benefit for gold cards. “When comparing credit cards, it makes more sense to look for the actual benefits and services you need,” explains Ralf Beyeler.

The costs of standard credit cards

Most Swiss credit card issuers charge a basic annual fee of 100 francs for their standard credit cards. Only a handful of issuers have cheaper cards. Standard credit cards are often referred to as classic or silver cards. Typically, standard credit cards include reward programs and insurance coverages.

Of the credit cards included in the analysis, Postfinance has the cheapest standard credit cards. Liberty card and Raiffeisen are next in line. Here too, differences in costs are huge. For the occasional user profile, the most expensive card offer costs more than twice as much as the cheapest card offer. For the frequent user profile, the difference is around 73 percent.

You can find the detailed results in table 2 in the PDF.

The costs of gold credit cards

Gold credit cards typically include more services than standard credit cards. Often, you get additional insurance, and the coverage is often better. Most issuers charge annual fees of around 200 francs, though some gold cards have lower annual fees.

As with standard credit cards, Postfinance leads with the lowest costs for gold cards as well. It is followed by Raiffeisen and Cornèrcard.

You can see the detailed results on table 3 in the PDF.

The cost of platinum credit cards

Platinum credit cards provide the most comprehensive range of services. Services vary between offers. In addition to various kinds of insurance, platinum cards may also include airport lounge access and concierge services, among other services.

Typically, the annual fee for platinum credit cards is around 500 francs, though there are cards in this class that cost around 200 francs per year. In many cases, platinum cards have relatively high income requirements. Because card offers vary broadly with regards to the type and scope of services they include, it is advisable to compare credit cards based on your specific needs.

Pay attention when making purchases from foreign merchants

Costs generated when you pay for purchases from foreign merchants are a major contributor to the costs of using a credit card. In addition to foreign transaction fees, unfavorable currency exchange rates can also add a substantial cost.

A study published by moneyland.ch in March 2026 shows that Swiss credit cards are more expensive than Swiss debit cards for foreign transactions. Debit cards from Bank WIR and the neobanks Alpian and Wise are particularly affordable, as the study shows.

Before traveling, tourists should familiarize themselves with these two important costs:

Useful tips for choosing the right credit card

When looking for the best credit card, it is important to think about how you will use your credit card. “If your main reason for having a credit card is to make payments, a no-annual-fee credit card that matches your needs is usually a good choice,” says Ralf Beyeler from moneyland.ch. If you also need insurance cover, then credit cards with annual fees are worth taking a look at.

The interactive credit card comparison on moneyland.ch makes finding the right card quick and easy.

Methodology

The Swiss Credit Card Study 2026 from moneyland.ch accounts for market-relevant credit cards from numerous Swiss credit card issuers.

The study includes cards from these issuers: Bonuscard, Cembra Money Bank, Cornèrcard, Migros Bank, Postfinance, Raiffeisen, Swisscard, Topcard, UBS, and Viseca. Many popular Swiss retailers partner with issuers to offer co-branded credit cards. Co-branded cards used in this study include American Express, Conforama, Coop, Ikea, Manor, Migros und Poinz.

Co-branded credit cards from Airlines are not included in the study, as the monetary value of airlines miles cannot be clearly determined.

These costs are accounted for in the analysis:

The analysis is based on these two user profiles:

The analysis does not account for special promotions like introductory annual fees and welcome bonuses.

Current Offers From Banks

Current Offers From Banks

Swissquote

Leading Swiss online bank with FINMA license

Free multicurrency account & low commissions

Access to more than 3 million products (shares, ETFs, crypto and more)

Yuh

No account fees

Banking partner: Swissquote

CHF 20 trading credit with code «YUHMONEYLAND»

Managed by Alpian

Up to CHF 50 investment fee credit

Customized portfolios

Unlimited access to wealth advisor

Swisscard Cashback Cards Amex

No annual fees

Two cards Amex & Visa/Mastercard

With cash back

UBS Banking for adults

Open and manage your account, savings account, and cards easily in the UBS Mobile Banking App

Plus KeyClub rewards program

50 CHF welcome gift

UBS Gold Credit Card

High card limit for more flexibility

Premium travel insurance included

Earn valuable KeyClub points with every payment

Deal of the Day

Deal of the Day  Swiss Trading Platform

Swiss Trading Platform

Swissquote

Leading Swiss online bank with FINMA license

Current Offers

Current Offers

Fiber & Sky Show

Fiber up to 2.5 Gbit/s & unlimited premium series

CHF 42.90/m for 6 months (then CHF 40.90/m)

Free activation (worth CHF 99)

Swisscard Cashback Cards Amex

No annual fees

Two cards Amex & Visa/Mastercard

With cash back

Swissquote

Leading Swiss online bank with FINMA license

Free multicurrency account & low commissions

Access to more than 3 million products (shares, ETFs, crypto and more)

Manor World Mastercard®

20% welcome discount + 10x points on your first purchase

Free extended warranty, travel and purchase insurance

Pay worldwide and collect points (even earn double points at Manor)

Managed by Alpian

Up to CHF 50 investment fee credit

Customized portfolios

Unlimited access to wealth advisor

UBS Banking for adults

Open and manage your account, savings account, and cards easily in the UBS Mobile Banking App

Plus KeyClub rewards program

50 CHF welcome gift

Generali

CHF 100.- Migros voucher upon conclusion

Death coverage

Premium guarantee: No increase

PKZ Insider Card Visa

Welcome Bonus of CHF 100

No annual fees forever

Double bonus with PKZ and up to 1% worldwide