Swiss Neobank Study 2026

Get a detailed overview of the Swiss Neobank Study 2026 sent to your email free of charge.

Online comparison service moneyland.ch analyzed the costs of neobanks available in Switzerland, as well as additional banks. The results show that a traditional Swiss bank is cheaper than all of the neobanks. Differences in the costs of foreign transactions are particularly large.

Neobanks market themselves as cheap and easy to use. Yuh, the most widely-used Swiss neobank, now counts 400,000 customers, while its closest competitor Neon has around 253,000 customers.

Making payments in foreign countries is one area in which neobanks are widely considered to be the cheapest option. But does that perception match the facts? The Swiss Neobank Study 2026 by online comparison service moneyland.ch compares neobanks available to Swiss consumers with other Swiss banks.

Currency exchange rates are a major cost factor

moneyland.ch hat die jeweils anfallenden Kosten pro Jahr berechnet. Grundlage ist ein Profil mit einem monatlichen Lohneingang, dem Bezahlen von Rechnungen und der Miete sowie einer intensiven Kartennutzung in der Schweiz (10’000 Franken pro Jahr) und im Ausland (je umgerechnet 2000 Franken in Euro, US-Dollar und thailändischen Baht). Zudem wird siebenmal an Bancomaten Bargeld bezogen.

For its analysis, moneyland.ch calculated the total annual banking costs. The calculations are based on a customer profile that includes: a monthly incoming salary; the payment of rent and other bills; local card payments in Switzerland totaling 10,000 francs; and the equivalent of 2000 francs spent with the card outside of Switzerland in euros, US dollars, and Thai baht.

Costs that result from unfavorable currency exchange rates are an important factor when making international transactions. For that reason, moneyland.ch accounted for markups above the interbank rates.

These are the cheapest neobanks

The study includes Swiss neobanks Alpian, Neon, Yuh, and Zak. It also includes Revolut and Wise, two foreign neobanks that do not have Swiss banking licences or Swiss depositor protection, but are available to Swiss consumers.

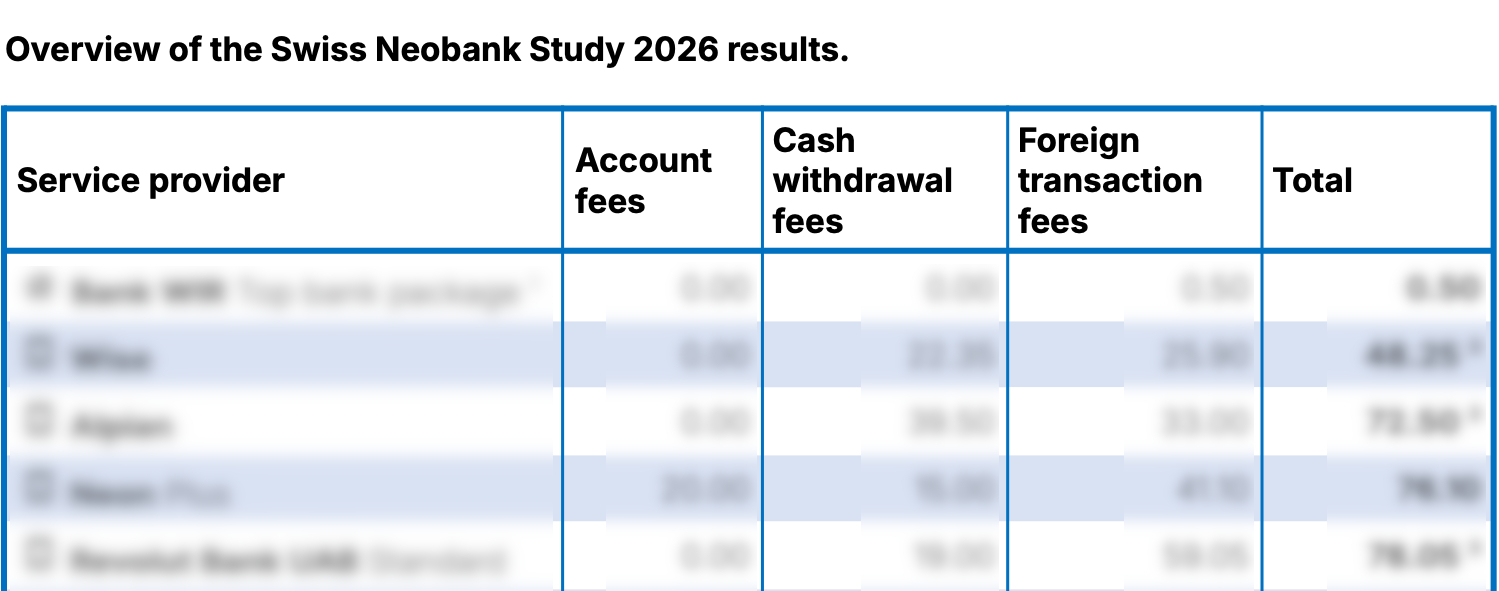

The cheapest neobank offers for consumers in Switzerland is Wise, with costs of 48.25 francs. Alpian takes second place (72.50 francs), followed by Neon Plus (76.10 francs), and Revolut Standard (78.05 francs). Yuh, the largest Swiss neobank, has total costs of 101.40 francs. The last places are occupied by two offers from Zak, with costs of 262.75 and 326.75 francs respectively.

It is important to note that Revolut and Wise do not give the user an individual Swiss bank account, which often makes them unsuitable for receiving Swiss salaries.

How do traditional banks compare to neobanks?

Many consumers wonder how neobanks actually compare with conventional banks in terms of costs. For that reason, moneyland.ch used the same methodology to analyze major conventional banks like UBS, Raiffeisen, Postfinance, and some cantonal banks, as well as Bank Wir and Swissquote.

A look at the graph makes it clear that neobanks largely dominate the ratings. But the cheapest bank of all is a traditional Swiss bank. In the combined comparison of both neobanks and conventional banks, Bank WIR sits at the top of the rankings, with costs of just 50 centimes per year. The neobank Wise, which took second place, costs nearly 48 francs more.

Of the other conventional Swiss banks, Swissquote (140.55 francs), the Zürcher Kantonalbank (149.25 francs), and Valiant (249.25 francs) are the next cheapest. These three cost more than all but one of the six neobanks included in the analysis.

The analysis also reveals big cost differences between banks. With costs of around 300 francs, Raiffeisen, Postfinance, and UBS are around twice as expensive as Swissquote and the Zürcher Kantonalbank. Bank Cler has the highest costs, at 412.75 francs.

High banking costs are easy to avoid

It is worth noting that the customer profile used for the analysis includes payments in foreign countries. This is important because affordable foreign transactions are a key feature in neobanks’ marketing campaigns. The differences in the cost of foreign transactions – which range from 50 centimes to 320.75 francs – are strongly reflected in the results.

Consumers can easily avoid high foreign transaction costs. “Even if you do not want to change your main bank, you could still consider using a cheaper service provider for payments outside of Switzerland,” recommends moneyland.ch financial expert Ralf Beyeler.

Investment and pillar 3a services

Swiss neobanks have focused primarily on payment cards, accounts, and savings solutions. But they are steadily adding new features. Alpina, Neon, Yuh, and Zak not offer services for investing in securities like stocks, ETFs, and mutual funds. Yuh and Zak recently joined Alpina and Neon in offering their own pillar 3a solutions.

A look at the Swiss Neobank Study 2026 compared to previous years shows how the Swiss neobank landscape has changed. The neobanks CSX, Coop Finance Plus, and Radicant have disappeared, as has the consumer offer from Kasparund. “The market has consolidated,” observes Ralf Beyeler from moneyland.ch. The consolidation was not driven by bankruptcies, but by deliberate withdrawals from the market. Swiss neobanks are considered to be secure.

Neobanks are not always the best solution

Some consumers are cautious about using neobanks, and moneyland.ch financial expert Ralf Beyeler understands the concerns. “Neobanks are not the most suitable banking solution for every consumer.” If personal contact at a branch office is important to you, then you should stick with a conventional bank. Consumers who prefer digital solutions are more likely to benefit from using neobanks.

Other considerations include the options for contacting the bank, the usability of mobile apps, the quality of customer service, and which banking services are offered. But in the case of Swiss neobanks, security is not a major concern, as all Swiss neobanks either have their own bank license or work with conventional banks that manage the actual bank accounts. Foreign neobanks like Revolut and Wise, on the other hand, are not covered by Swiss bank depositor protection.

*Information about Revolut applies to the Revolut Bank UAB.

Get a detailed overview of the Swiss Neobank Study 2026 sent to your email free of charge.

Swiss Neobank Study 2026

Methodology

The calculations are based on these assumptions:

Service providers were asked to provide their currency exchange rates on these dates in early 2026: January 29 and 30; February 3, 4, 5, 6, 9, 10, 11, 16, 17, 18, 19, and 20. The figures provided were used to calculate an average exchange rate, which was then compared to the interbank rate published by Oanda.

The following service providers were included in the analysis:

For conventional Swiss banks, the analysis always accounts for the cheapest offer from each bank. For neobanks, all offers are accounted for.

The rankings are based on calculations for a specific customer profile, and can differ if a different profile is used. The individual cost criteria are rounded to the nearest 5 centimes. Possible complementary services like consultation or insurance are not accounted for.

Twint is not accounted for because it cannot be used to make payments outside of Switzerland.

You can find the moneyland.ch Swiss Neobank Study for previous years here: 2022, 2023, 2024, 2025.